What is a Credit Score?

A credit score is a number generated by a mathematical formula that is meant to predict credit worthiness. Credit scores are typically presented on a numerical scale; the score range and model may vary by bureau and product. Credit scores typically range from 300-850. The higher your score is, the more likely you are to get a loan. The lower your score is, the less likely you are to get a loan. If you have a low credit score and you do manage to get approved for credit then your interest rate will be much higher than someone who had a good credit score and borrowed money. Therefore, having a high credit score can save many thousands of dollars over the life of your mortgage, auto loan, or credit card.

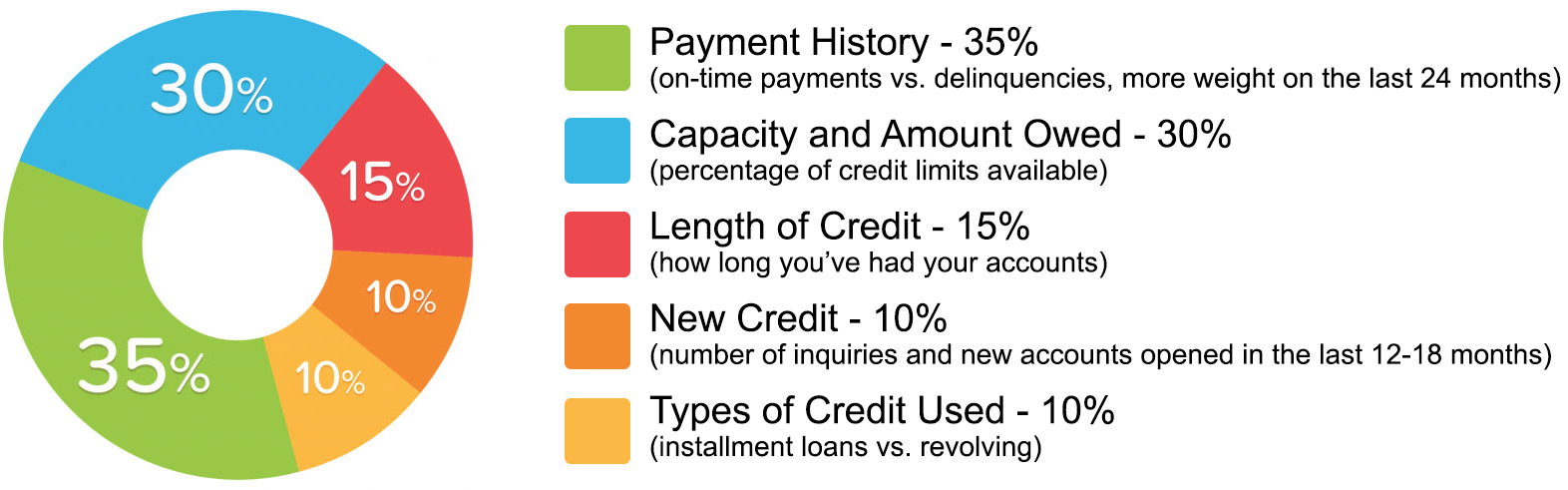

What affects your Credit Score?

Get Your Credit Report (Jamaica)

Request your report directly from Jamaica’s credit bureaus:

EveryData Jamaica: https://jm.everydata.com/consumer-credit-report

CRIF Jamaica: https://www.crif.com.jm/consumers-area/get-a-copy-of-your-credit-report/

Note: Links provided for convenience. Reports are requested directly from the bureaus’ official portals.

We will help you to dispute negative items in your payment history.

- We help you identify potentially inaccurate or incomplete payment history items and prepare dispute/support documentation for submission through the appropriate channels, based on your instructions and authorization. It is important to review your credit report for accuracy and completeness. If you find information you believe is inaccurate or incomplete, you can register a dispute with the credit bureau; dispute investigations may take up to fourteen (14) days depending on the bureau and the nature of the query.

- We help you reduce credit utilization risk with a practical balance-management plan aligned to your income and obligations.

- We help you review credit inquiries for accuracy and guide dispute steps with supporting documentation where an inquiry appears unauthorized or inaccurate.

Jamaica note: Consumers in Jamaica can request their credit report and register disputes through local credit bureaus operating in Jamaica, including CRIF Information Bureau Jamaica and EveryData Jamaica, using their dispute processes. - Deliverables Guarantee: If we do not provide the agreed service deliverables for the package purchased (for example: assessment, action plan, and dispute-support documentation where applicable), you may request a review by emailing creditclinccl@gmail.com within fourteen (14) calendar days of the deliverable due date. Refund eligibility does not apply where deliverables were provided and a refund is requested based on outcomes, third-party decisions, or failure to follow agreed steps.

In addition to starting the credit dispute process with you, what can I do to help raise my credit score?

Pay all of your bills on time, every time. This includes your utility bills, mortgage and auto payments, and all of your revolving lines of credit like credit cards. Check your credit report at least once a year. You can find out how to challenge bad information on your credit report here.

Never charge more than 30% of the available balance on any of your credit cards. Banks like to see a nice record of on-time payments, and several credit cards that are not maxed-out. If you are carrying high balances on your credit cards, then make paying them down below 30% a priority. Do use your credit cards – Many people who make mistakes with their credit believe that the best way to fix things is to never use credit again. If you are afraid that you cannot handle your credit cards correctly then the best policy is probably this one: Run only your utility bills on your credit cards each month, and then pay the balance in full by the due date. This ensures that your utility bills get paid on time automatically, and as long as you keep the habit of paying off your credit card balance each month your score will continue to go up. Leave the credit cards locked in a safe or drawer at home.

Keep your accounts open as long as possible – Even if you are no longer charging on the card. The best policy is to keep those unused accounts open, blow the dust off your card every few months to make a small purchase, then pay it off. How long each of your accounts have been active is a major factor in your credit score.

Remember that this all takes time – Following the above steps consistently over a long period of time will increase your credit score and allow you to qualify for better loans and lower interest rates. Repairing your credit score does not happen overnight, so if you do these things for a few months and do not see a large increase in your score, do not give up. They are all habits that you will want to maintain throughout your life, as they will help you to keep your finances and lines of credit under control.

Never charge more than 30% of the available balance on any of your credit cards. Banks like to see a nice record of on-time payments, and several credit cards that are not maxed-out. If you are carrying high balances on your credit cards, then make paying them down below 30% a priority. Do use your credit cards – Many people who make mistakes with their credit believe that the best way to fix things is to never use credit again. If you are afraid that you cannot handle your credit cards correctly then the best policy is probably this one: Run only your utility bills on your credit cards each month, and then pay the balance in full by the due date. This ensures that your utility bills get paid on time automatically, and as long as you keep the habit of paying off your credit card balance each month your score will continue to go up. Leave the credit cards locked in a safe or drawer at home.

Keep your accounts open as long as possible – Even if you are no longer charging on the card. The best policy is to keep those unused accounts open, blow the dust off your card every few months to make a small purchase, then pay it off. How long each of your accounts have been active is a major factor in your credit score.

Remember that this all takes time – Following the above steps consistently over a long period of time will increase your credit score and allow you to qualify for better loans and lower interest rates. Repairing your credit score does not happen overnight, so if you do these things for a few months and do not see a large increase in your score, do not give up. They are all habits that you will want to maintain throughout your life, as they will help you to keep your finances and lines of credit under control.

How long will certain items remain on my credit file?

- Delinquencies (30- 180 days): A delinquency may remain on file for seven years; from the date of the initial missed payment.

- Collection Accounts: May remain seven years from the date of the initial missed payment that led to the collection (the original delinquency date). When a collection account is paid in full, it will be marked as a "paid collection" on the credit report.

- Charge-off / Written-off Accounts: Where an account is written-off or referred for collection, it may continue to appear on your credit file as part of your account history, generally within the up to seven (7) years reporting window after the account is closed/settled (or final payment), consistent with local bureau reporting policies.

- Closed Accounts: Closed accounts are no longer available for further use and may or may not have a zero balance. Closed accounts with delinquencies remain for seven years from the date they are reported closed, whether closed by the creditor or by the consumer. However, the delinquency notation will be removed seven years after the delinquency occurred when pertaining to late payments. Positive closed accounts may continue to appear as part of your credit history until they age off, and credit reports generally do not include credit information older than seven (7) years after a loan is closed.

- Lost / Stolen Credit Card: If there are no delinquencies, the account may continue to appear on your credit file as part of your revolving credit history until it is closed and ages off, generally within the up to seven (7) years reporting window after closure. Any delinquencies that occurred before the card was reported lost may also remain within that reporting window.

- Bankruptcy / Insolvency: Bankruptcy and insolvency-related court records may appear under Public Records on a Jamaican credit report. As a general guide, credit bureaus typically report up to seven (7) years of credit history, and credit reports generally do not include credit information older than seven years after a loan is closed; confirm the specific treatment with the relevant credit bureau.

- Judgments: Information about a judgment is generally not disclosed if it was given more than seven (7) years before the date the information is provided, except in limited circumstances permitted by the Credit Reporting Act; confirm any exception case with the relevant credit bureau.

- Taxes / Tax-related liens (where applicable): Tax liens and similar tax-related filings may appear under Public Records on a Jamaican credit report. As a general guide, reporting is typically limited to up to seven (7) years of history; confirm the specific treatment with the relevant credit bureau.

- Inquiries: Most credit inquiries may remain visible on your credit report for up to two (2) years, depending on the credit bureau and the type of inquiry. Some inquiries (for example, pre-approved offers or employment-related checks, where applicable) may be visible only on reports you request for yourself. For the most accurate treatment, confirm with the relevant credit bureau.

Information that should not appear in a credit report:

- Medical/health information (sensitive personal data) should not appear for credit reporting except where lawful and appropriately safeguarded (often with explicit consent).

- “Chapter 11” bankruptcy references are not applicable in Jamaica; only accurate bankruptcy/insolvency public-record information should be reported within the applicable period.

- Credit information older than seven (7) years after an account is closed or finally settled (subject to limited exceptions and bureau rules).

- Sensitive demographic data (e.g., race/ethnic origin) and non-credit-relevant details (e.g., marital status) should not appear without a clear lawful purpose and required consent.